A Senate panel released a damning report accusing the likes of Goldman Sachs of engaging in massive conflicts of interest, contaminating the U.S. financial system with toxic mortgages and undermining public trust in U.S. markets in the months leading up to the financial crisis.

Just when you thought Washington lawmakers were over that whole financial crisis thing, Senator Carl Levin, D-Mich., and Senator Tom Coburn M.D., R-Okla, blast Wall Street in a 635-page report stemming from a 2-year bipartisan investigation on the key causes of the crisis.

The report comes at a time when much of the feeling from lawmakers in Washington is that Wall Street is being over-regulated by the new Dodd-Frank rules.

The report from the Senate’s Permanent Subcommittee on Investigations however takes an opposite view by citing internal documents and private communications of bank executives, regulators, credit ratings agencies and investors to depict an industry that was rife with conflicts of interest and reckless during the mortgage surge.

Senator Levin said in the release yesterday:

“Using emails, memos and other internal documents, this report tells the inside story of an economic assault that cost millions of Americans their jobs and homes, while wiping out investors, good businesses, and markets,” said Levin. “High risk lending, regulatory failures, inflated credit ratings, and Wall Street firms engaging in massive conflicts of interest, contaminated the U.S. financial system with toxic mortgages and undermined public trust in U.S. markets. Using their own words in documents subpoenaed by the Subcommittee, the report discloses how financial firms deliberately took advantage of their clients and investors, how credit rating agencies assigned AAA ratings to high risk securities, and how regulators sat on their hands instead of reining in the unsafe and unsound practices all around them. Rampant conflicts of interest are the threads that run through every chapter of this sordid story.”

The report takes specific issue with the way Goldman Sachs touted investments to clients on one end but bet against them on the other. A similar accusation against Goldman by the SEC lead to a $550 settlement last year, but Levin and his team don’t think that punishment fits the crime. From the report:

When Goldman Sachs realized the mortgage market was in decline, it took actions to profit from that decline at the expense of its clients. New documents detail how, in 2007, Goldman’s Structured Products Group twice amassed and profited from large net short positions in mortgage related securities. At the same time the firm was betting against the mortgage market as a whole, Goldman assembled and aggressively marketed to its clients poor quality CDOs that it actively bet against by taking large short positions in those transactions.

New documents and information detail how Goldman recommended four CDOs, Hudson, Anderson, Timberwolf, and Abacus, to its clients without fully disclosing key information about those products, Goldman’s own market views, or its adverse economic interests. For example, in Hudson, Goldman told investors that its interests were “aligned” with theirs when, in fact, Goldman held 100% of the short side of the CDO and had adverse interests to the investors, and described Hudson’s assets were “sourced from the Street,” when in fact, Goldman had selected and priced the assets without any third party involvement.

New documents also reveal that, at one point in May 2007, Goldman Sachs unsuccessfully tried to execute a “short squeeze” in the mortgage market so that Goldman could scoop up short positions at artificially depressed prices and profit as the mortgage market declined.

This isn’t the first time Levin is gunning for Goldman. Back in April 2010, the Senator had a memorable back-and-forth with a Goldman executive during a testimony where the two discussed a “shitty deal” the firm was selling to clients.

This isn’t the first time Levin is gunning for Goldman. Back in April 2010, the Senator had a memorable back-and-forth with a Goldman executive during a testimony where the two discussed a “shitty deal” the firm was selling to clients.

In fact, Levin is referred to that very testimony yesterday saying he doesn’t think Goldman executives were being truthful about its activity, and that he would refer the testimony to the Department of Justice and the Securities and Exchange Commission for possible criminal investigations.

“In my judgment, Goldman clearly misled their clients and they misled the Congress,” he said.

Goldman isn’t alone in feeling Levin’s wrath though. The report also points to Deutsche Bank AG (DB) saying the Frankfurt-based company created a $1.1 billion CDO with assets that its traders referred to as “crap” and “pigs” but then attempted to sell “before the market falls off a cliff.”

Not even credit rating agencies are spared in this report which concluded that “the most immediate cause of the financial crisis was the July 2007 mass ratings downgrades by Moody’s and Standard & Poor’s that exposed the risky nature of mortgage-related investments that, just months before, the same firms had deemed to be as safe as Treasury bills.”

Here’s more:

Internal emails show that credit rating agency personnel knew their ratings would not “hold” and delayed imposing tougher ratings criteria to “massage the … numbers to preserve market share.” Even after they finally adjusted their risk models to reflect the higher risk mortgages being issued, the firms often failed to apply the revised models to existing securities, and helped investment banks rush risky investments to market before tougher rating criteria took effect.

They also continued to pull in lucrative fees of up to $135,000 to rate a mortgage backed security and up to $750,000 to rate a collateralized debt obligation (CDO) – fees that might have been lost if they angered issuers by providing lower ratings. The mass rating downgrades they finally initiated were not an effort to come clean, but were necessitated by skyrocketing mortgage delinquencies and securities plummeting in value. In the end, over 90% of the AAA ratings given to mortgage-backed securities in 2006 and 2007 were downgraded to junk status, including 75 out of 75 AAA-rated Long Beach securities issued in 2006.

When sound credit ratings conflicted with collecting profitable fees, credit rating agencies chose the fees.

Among the 19 recommendations from the panel on how to handle the problems is one suggestion that asks the SEC to rank credit rating agencies according to the accuracy of their ratings.

At this stage, do we think the SEC can handle that?

Source: Forbes

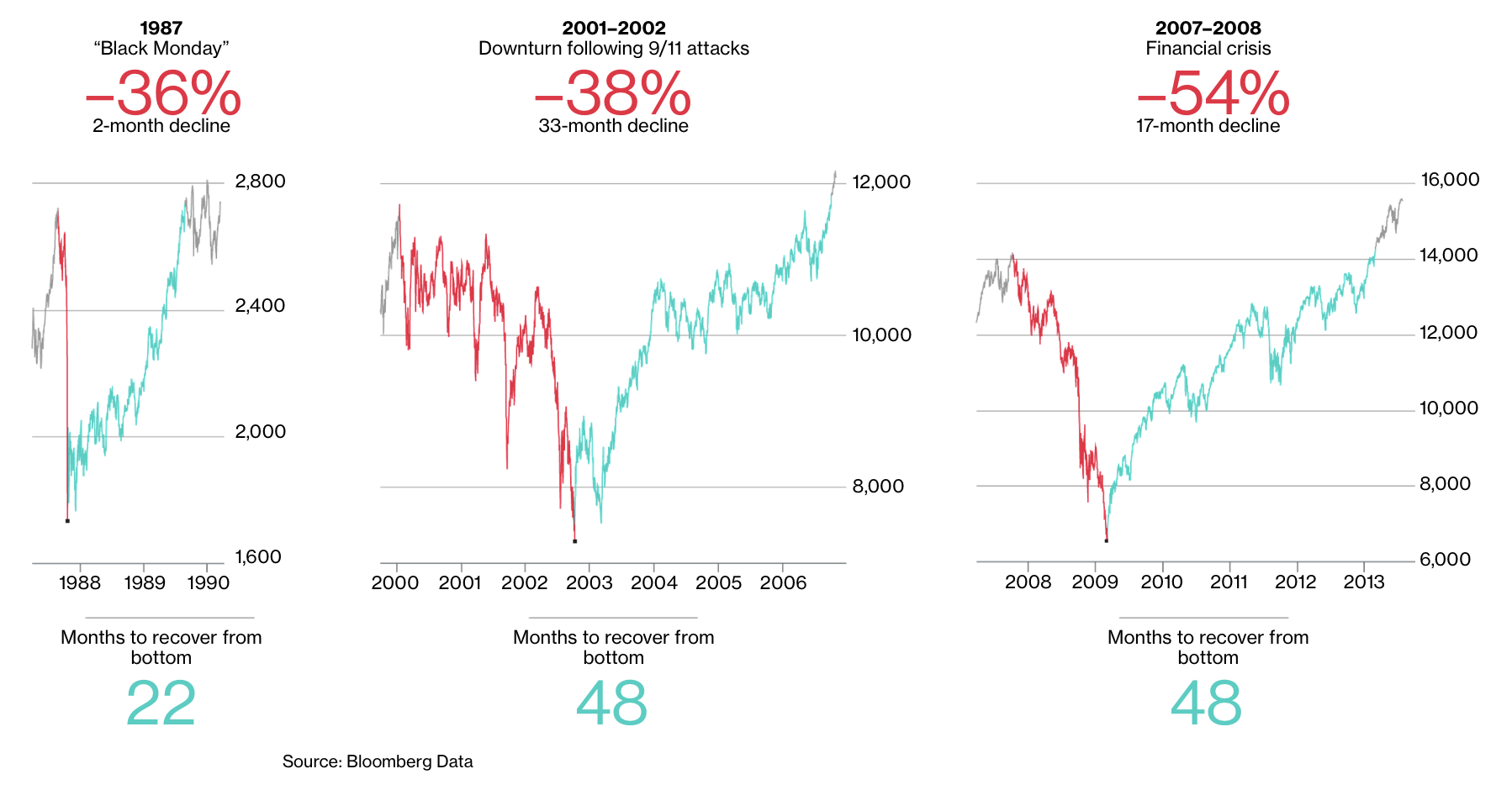

Johnny Liberty, Editor’s Note: This is exactly why we stayed out of the markets due to the possibility of extreme fluctuation due to events beyond our control (e.g., coronavirus). This market adjustment was long overdue and the Power Structure took advantage of the “panic” in partnership with Big Media to remove trillions of dollars of value.

Johnny Liberty, Editor’s Note: This is exactly why we stayed out of the markets due to the possibility of extreme fluctuation due to events beyond our control (e.g., coronavirus). This market adjustment was long overdue and the Power Structure took advantage of the “panic” in partnership with Big Media to remove trillions of dollars of value.

On March 5, 2012, the Oregon Legislature passed a sweeping series of changes to its trust deed foreclosure law,

On March 5, 2012, the Oregon Legislature passed a sweeping series of changes to its trust deed foreclosure law,

By Halah Touryalai

By Halah Touryalai By Kevin G. Hall

By Kevin G. Hall